Retirement Planning

Importance of retirement planning

One of the biggest financial mistakes people make is failure to set aside money for retirement. This is especially true of younger people for whom retirement seems a long way away.

The fact is, your retirement is probably less stable than ever before. Pensions are mostly a thing of the past, and Social Security is no longer a sure bet. This means that you have to rely on yourself to provide for your retirement. And this means retirement planning.

Retirement planning begins with setting goals and putting together a plan to achieve them. If you haven't made retirement planning a priority, make it one now. There are many options available from IRAs to 401(k)s to special plans for the self-employed. Check with a financial planner, or do your own research, and find a way determine what you need to do now so that you are secure in your future.

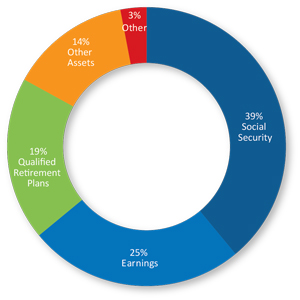

Sources of retirement income

Retirement income usually comes from three major sources – Social Security, qualified retirement plans such as IRAs and 401(k)s and savings and investments. If you plan to continue working part-time during your retirement, you can consider these earnings as well.

Expand All

Social Security (35% of income in retirement)1

Social Security remains the most common source of income for people age 65 and older, although it was never intended to replace 100% of one’s income in retirement. About 86% of seniors receive monthly checks for an average of $14,681 annually.2 You can collect Social Security benefits in retirement based on your own work record or as the spouse of a worker. The amount of your benefit is based on your covered earnings during your working years.

Social Security remains the most common source of income for people age 65 and older, although it was never intended to replace 100% of one’s income in retirement. About 86% of seniors receive monthly checks for an average of $14,681 annually.2 You can collect Social Security benefits in retirement based on your own work record or as the spouse of a worker. The amount of your benefit is based on your covered earnings during your working years.

The earliest age at which benefits are available (at a reduced rate) is 62. Full benefits depend on your year of birth. If you were born before 1938, you can receive full benefits at age 65. The age needed to receive full benefits gradually rises until you reach age 67.

The future of Social Security is uncertain at best. Significant changes to the program may be needed in order to deal with the country’s budget deficit.

Earnings from employment (34% of income in retirement)3

About one-third of men and one-fourth of women aged 65 to 69 are still in the labor force.4 Some of them are delaying retirement, and others are working for other reasons. Access to employment and earnings can make a big difference in your retirement income.

You should remember that until you reach age 70, there’s a limit on how much you can earn before Social Security benefits are reduced. Check with your local Social Security office for the amount you’re allowed to earn before your benefits are reduced, and consider the trade-off between reduced benefits and increased income from earnings. Don’t forget to consider work-related expenses like transportation, meals, and special clothing.

Qualified retirement plans (17% of income in retirement)5

Pensions used to be the most common retirement plans provided by employers, but no more. Traditional pensions have given way to defined-contribution retirement plans such as 401(k)s, 403(b)s, 457s and SIMPLE IRAs.

Your employer may or may not choose to match some or all of the earnings you contribute to your plan. Employer matching depends on calculations based on employees participating equally in the plan. The benefits of these plans differ according to who participates, the amount you’re allowed to contribute, and how the investments perform.

One advantage of defined-contribution plans is that you usually have control over how your money is invested. Plus, you can take your plan with you if you change jobs.

Savings and investments (11% of income in retirement)6

The final piece of your retirement income will come from personal savings and investments. These include personally owned retirement accounts such as IRAs, annuities, banks savings, CDs or other investments.

Other sources (3% of income in retirement)7

1,3,5,6,7SSA Publication No. 13-11727, 2014

2SSSA Monthly Statistical Snapshot, July 2015

4US Census Bureau, 2013

Retirement products

Expand All

Annuities

An annuity is a contract between you and an insurance company where you make a single payment or a series of payments. In return, the insurer makes regular payments to you beginning immediately or at a later date. Annuities offer tax-deferred earnings growth and may include a death benefit that will pay your beneficiary a guaranteed minimum amount.

There are generally two types of annuities: fixed and variable. In a fixed annuity, the insurance company guarantees that you will receive a minimum rate of interest during the time your account is growing. The insurer also guarantees that the periodic payments will be a guaranteed amount per dollar in your account. These payments may last for a definite period, such as 20 years, or an indefinite period, such as your lifetime or the lifetime of you and your spouse.

In a variable annuity, you can choose to invest your payments in a range of different investment options, typically mutual funds. The rate of return on your purchase payments, and the amount of periodic payment you will eventually receive, will vary depending on the performance of your investments.

Asset Transfer

Many retirees are concerned about their family’s financial future and wish to transfer a portion of their estates to them upon death. By allocating a portion of their assets to a single premium whole life insurance policy, retirees can immediately increase the value of their estate while providing their beneficiaries with an inheritance that’s potentially free of federal income tax. Additionally, this product provides a guaranteed lifetime death benefit with access to cash values for financial emergencies.

Retirement income maximization using life insurance

While pensions may be a thing of the past for most people, there are still many people eligible to receive benefits from old defined benefit plans that their employer may no longer be maintaining for newer employees. These participants typically have to make a decision before retiring regarding what type of benefit they will receive: a “life only” benefit for the life of the plan participant or a “joint and survivor” benefit that pays a benefit for as long as the plan participant and their spouse live.

The life only benefit is usually larger. Therefore, the participant must choose between receiving a larger lifetime benefit with no survivor benefit, or a reduced lifetime benefit but with a continuing income for the surviving spouse.

However, the participant can get the best of both worlds by choosing the larger life only benefit and purchasing life insurance to replace the survivor benefits. This strategy provides the participant with the maximum pension income available, provides for the surviving spouse, and potentially provides emergency funds not otherwise available.

Retirement savings products

Two of the most popular forms of retirement investing are the 401(k) and the IRA. Despite their popularity, there is still some confusion about them.

A 401(k) is offered by your employer. You contribute a certain percentage of your salary into an account, and your employer usually offers to match your contribution up to a certain percentage. You can contribute beyond the match point depending on your salary. You can usually allocate your funds into a variety of investments. The money you contribute is usually before-tax money and it grows tax-deferred. When you turn 70 ½ , you must begin making minimum withdrawals unless you are still working, and these withdrawals are taxed.

IRA stands for Individual Retirement Account, and as the name implies, it’s a sole ownership account. There are many different types of IRAs, and you should speak to a financial expert or research different options before deciding on which one is right for you.

A Traditional IRA is established with after-tax funds that grow tax-deferred until they are withdrawn. Traditional IRA yearly contributions can usually be claimed as a tax deduction. A Roth IRA allows you to use after-tax funds, but they cannot be claimed on your taxes. However, you can usually make tax-free withdrawals.

Distribution of assets

Consult an Insurance Professional

Comments contained in this website reflect our understanding of current tax law. However, the laws are subject to different interpretations and changes. Our agents do not provide tax advice. Please consult with your tax advisor about your personal situation.